UK Chancellor Rachel Reeves is preparing for a TV round this morning to reassure us there is no fuel shortage. Its like when a stranger knocks on your front door and says”Don’t worry” and you know you should be very very worried.

We’ve all seen the headlines about the UK’s “two-day” gas reserve. It’s the energy equivalent of realising you’re down to the last two squares of loo roll while the shops are shut. But as we move toward April 2026, the reality is more nuanced, more urgent, and frankly, a bit more “Hunger Games” than we’d like for anyone managing a business, or even planning a hot shower.

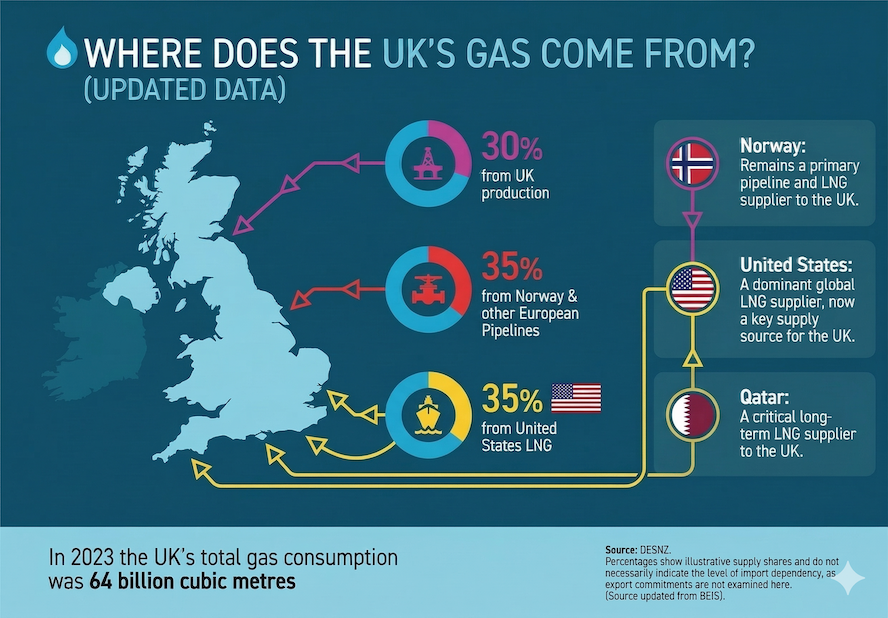

For the last few years, we’ve treated US LNG as our dependable American cousin who shows up to the party with a big wooden keg just as the beer runs out. But following the recent Jones Act Waiver, that cousin has now granted themselves the option to lock the front door, drink the kegs themselves, and then burn the empties to keep their own house warm.

The rumour mill is spinning faster than a faulty smart meter: the US is eyeing “export throttles” to protect domestic prices. If those taps turn even slightly, the UK is looking at a 15–20% supply hole opening up in less than 30 days. We aren’t just losing a supplier; we’re losing our safety net.

For the average household, the shortage won’t feel like a blackout—it’ll feel like a mugging.

-

THE REALITY: We were all looking forward to that 7% Price Cap drop in April. It was the one glimmer of hope in a bleak fiscal year. That hope is now under extreme threat.

-

THE RESULT: If US supply is cut, the government won’t let your radiators go cold (that’s PR suicide), but they will make you pay for the privilege. Expect “Emergency Energy Levies” to be slapped onto bills by summer. We’ll be forced to outbid Asia for the few remaining Qatari tankers that are brave enough to dodge the chaos in the Strait of Hormuz. It’s essentially a global auction where the prize is “not freezing.”

This is where the “stiff upper lip” starts to tremble. Unlike homes, industry is the national “buffer.” In the energy world, “buffer” is just a polite term for “the first people we throw overboard.”

-

DEMAND SIDE RESPONSE: If you’re running a high-intensity site—chemicals, glass, steel—get ready for the “Load Shedding” requests. It sounds like a trendy new minimalist lifestyle, but it actually means your local grid operator calling to ask if you’d mind turning off the factory for a bit.

-

THE COST OF STEAM: For gas-intensive manufacturing, the “marginal molecule” of gas will likely cost 3-4x the 2025 average. We are reaching a point where the math simply stops working. Many sites will find it cheaper to break their supply contracts and halt production entirely than to keep the furnaces running. When it’s more profitable not to make things, you know the system is in a fever dream.

We are currently staring down the barrel of the “Late April Chill.” It’s a classic British tradition: the moment you think it’s safe to put the duvet away, the Arctic sends us a parting gift.

If we hit a serious cold snap in 30 days without US LNG as a backstop, our storage won’t just be “critically low”—it will be a vacuum. We’ve spent years patting ourselves on the back for moving away from Russian gas, only to find we’ve traded a pipeline for a fleet of ships that can be diverted with a single executive order from Washington.

THE BOTTOM LINE

This isn’t 2022. We don’t have the same reserves, and we don’t have the same friends. The reliance we built on US LNG has become our greatest strategic vulnerability.